Non-recourse invoice factoring: What B2B marketplaces should know

Learn the difference between non-recourse and recourse factoring, what each option means for your business in terms of credit risk, and what to ask when evaluating invoice financing providers.

Modern B2B marketplaces are under pressure to offer longer payment terms to buyers. But as net 30, 60, and even 90 are great for buyers, sellers are left waiting months to get their outstanding invoices settled.

This cash flow strain makes it harder for sellers to cover operating costs and limits how much they can sell. As a result, they’re likely to seek out competitor marketplaces with faster payments in place, and the transaction volume on your own platform stalls.

The issue, though, isn’t buyers who pay later – it’s outdated payment and financing infrastructure that forces sellers to stretch their cash, even when they can’t afford to.

At Aria, we’ve heard the same story from marketplaces over and over: sellers tell them, “If I were paid twice as fast, I could sell three or four times more.” Clearly, the demand for faster payments is there – but marketplaces often lack the right funding solutions to offer cash advances without taking on risk.

Embedded invoice factoring is one straightforward way to fix this: sellers get early payment on approved invoices while buyers keep their regular terms. But it also raises a critical question: Who carries the risk when a buyer doesn’t pay?

That question is the difference between recourse and non-recourse invoice factoring.

In this article, we’ll cover:

- Recourse vs. non-recourse invoice factoring: What changes for your business

- What to ask when evaluating a non-recourse invoice factoring solution

- How embedded invoice financing works with Aria

- Why choose Aria as your non-recourse invoice factoring partner

- How Aria replaced 20 factoring partners with one unified solution for Job&Talent

Want to see how your marketplace can leverage non-recourse invoice financing? Schedule a free demo with Aria.

Recourse vs. non-recourse invoice factoring: What changes for your business

Before we get into the differences between the two types of factoring, let’s quickly touch on how invoice factoring works: in a nutshell, the finance provider advances payment to a seller based on approved invoices, with the understanding that the provider will be repaid once the buyer settles.

The key difference between recourse and non-recourse factoring, then, comes down to what happens if a buyer doesn’t pay.

| Recourse Factoring | Non-Recourse Factoring | |

| Who bears bad-debt risk? | Marketplace or the supplier | Factoring provider (within agreed terms) |

| Who manages collections? | Often marketplace or the supplier | Factoring provider |

| Fees | Typically lower | Typically higher |

| Eligibility requirements | Less strict | More stringent credit checks |

Recourse factoring means the marketplace or the seller keeps the risk of unpaid invoices. As part of the factoring agreement, the party that issued the invoice to the buyer must repay the factor if a buyer doesn’t pay.

For example, imagine a seller invoices a buyer for £10,000 with net-90 payment terms. The seller turns to a recourse factoring provider for early payment. If approved, the provider advances up to 95% of the £10,000 to the seller upfront (£9,500), expecting to be repaid once the buyer settles the invoice. However, if the buyer goes bankrupt and doesn’t pay, the seller must return the £9,500 to the factoring provider.

In recourse factoring, the seller (or marketplace, depending on the model) is often also responsible for chasing invoices and handling debt collections. The upside is that recourse solutions typically charge lower factoring fees than non-recourse, largely because the provider bears less risk.

Non-recourse factoring, on the other hand, shifts the risk of non-payment to the factoring provider. If a buyer goes bankrupt and cannot pay, the factoring company absorbs the loss and requires no repayment from the seller or marketplace.

Note that the factor won’t cover all scenarios where a buyer doesn’t pay. Non-recourse agreements typically cover buyer insolvency or bankruptcy within a defined period, but not disputes or late payments because of disagreements over product or service quality.

Because they take on more risk, non-recourse factoring providers tend to run more stringent credit checks and selectively approve invoices based on buyer creditworthiness. They also handle collections, which saves you and your suppliers time and administrative headaches.

In terms of cost, non-recourse factoring comes with slightly higher fees to cover the extra risk and work the provider takes on. At Aria, we’ve found many businesses see the premium as worth it.

What to ask when evaluating a non-recourse invoice factoring solution

Non-recourse invoice factoring isn’t a one-size-fits-all service. Different providers handle risk, validation, and collections in very different ways.

Before committing, it’s important to understand the details. Here are some key questions to ask when looking for a non-recourse invoice factoring solution:

1. When does non-recourse protection apply?

Not all non-recourse agreements cover every type of non-payment. With some providers, protection only kicks in if a buyer becomes insolvent within a defined timeframe, while others cover late payments as well. Generally, commercial disputes are excluded.

Some providers may cover additional scenarios, though, so make sure to ask for a clear breakdown of which scenarios are included and when liability might shift back to you or your sellers. This ensures there are no surprises down the line and helps you understand the coverage’s true value.

2. How are credit decisions made?

Ask your provider how they evaluate buyers:

- Do they use real-time credit scoring, historical payment data, or a combination?

- How often are these assessments updated?

- Are credit limits fixed, or do they adjust dynamically based on buyer behaviour?

- Can you request a manual re-evaluation of a credit limit?

It’s also worth asking whether the provider serves small business suppliers or only larger, high-volume accounts. This is because making financing accessible to more of your sellers can widen adoption across your marketplace. Better-funded suppliers can sell more – which ultimately brings in more buyers.

3. How does the validation process work?

Invoice validation is a critical step to reduce disputes and ensure funding is accurate. Some solutions require multiple manual checks, buyer confirmations, or back-and-forth approvals, which can delay cash flow.

Look for a provider that streamlines validation: automated invoice checks and digital confirmations require little manual intervention and can cut funding timelines. Faster validation also means sellers get paid sooner, and your marketplace stays competitive.

4. How are collections handled?

Ask whether the provider manages collections on your behalf and how they interact with buyers. Do they handle disputes professionally? Are communications compliant and brand-safe?

The ideal provider acts as an extension of your team and handles collections without damaging your seller relationships or reputation. At Aria, for instance, we organise workshops with our partners during the implementation phase to agree on messaging and timing of collections.

5. Can the solution be embedded into your product?

For marketplaces or platforms with more complex payment flows, standalone factoring isn’t always enough. This is because it often operates outside the platform’s core infrastructure.

Ask whether the solution can be embedded into your existing workflows, enabling sellers to request early payment directly within your platform. This turns factoring into a seamless, built-in feature, improving customer retention.

Consider the provider’s white-label capabilities as well. Would they empower you to customise branding and workflows so that the experience feels like part of your platform?

6. How difficult is integration, and how long does it take?

Even the best non-recourse factoring solution can lose its advantage if it takes months to set up or requires significant operational workarounds. Ideally, integration should be straightforward, minimise manual work, and enable your marketplace to scale quickly as demand grows.

Ask whether the provider offers flexible API options or only a plug-and-play solution. How long does implementation take? What internal resources are required?

Also look for features like:

- Sandbox environments

- Comprehensive and clear developer documentation

- Testing support

How embedded invoice financing works with Aria

Aria is an embedded, non-recourse invoice financing solution built specifically for B2B marketplaces and platforms. With a €2 billion financing capacity and over 65+ live clients, we help marketplaces offer faster seller payouts without taking on credit risk or disrupting existing buyer payment terms.

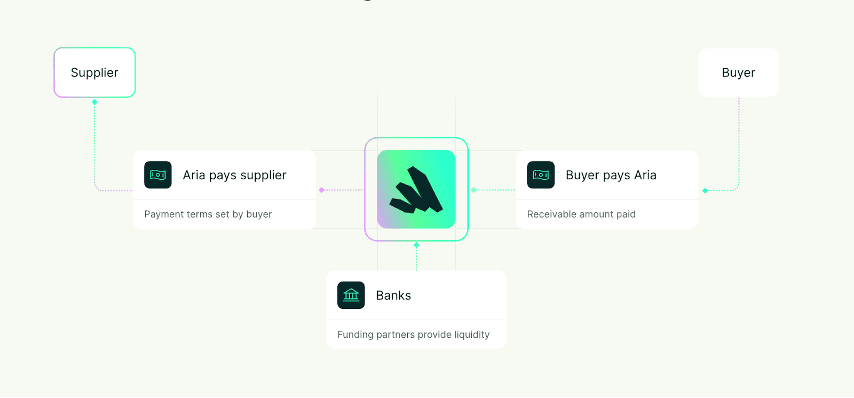

Here’s how Aria fits into the payment process on a marketplace:

- A business buyer registers with Aria directly on your marketplace. There’s no redirection to a third-party website. Everything happens within your product, creating a seamless experience for buyers and sellers alike.

- Aria issues a credit limit for the buyer. Behind the scenes, our payment and financing APIs assess solvency, verify identities (KYC/KYB), check for fraud, and determine eligibility for instant financing. These risk checks are fully automated, with 92% of decisions made instantly. Still, we’re flexible. If a key buyer needs a higher limit, we can review it with you.

- Once approved, buyers check out as usual, getting the payment terms they prefer.

- On the supplier side, sellers can request instant payment for eligible invoices based on the buyer’s credit limit. If your marketplace operates an intermediary model and invoices buyers directly, you can request payment.

- After the invoice is validated, Aria releases funds – often within 24 hours – to your sellers (or to you).

The buyer then pays Aria the full invoice amount according to the original payment terms.

Why choose Aria as your non-recourse invoice factoring partner

As a non-recourse invoice financing provider, Aria offers advanced payments of up to 100% of the invoice value, often within 24 hours. We take on the credit risk, so both you and your suppliers are fully protected if a buyer defaults.

Aria also handles late payments and collections. We manage outreach professionally and provide clear terms and conditions to help resolve disputes when they arise. In most cases, collections are handled seamlessly in the background without disrupting buyer or supplier relationships.

Here’s what partnering with us empowers you to do:

Serve suppliers of all sizes and enable faster business growth

While large, financially mature suppliers can often turn to banks for financing, smaller, local suppliers usually can’t. Costly to underwrite manually, they often get left behind. Yet these long-tail suppliers are often the backbone of a marketplace because they drive variety and growth.

Aria does things differently by underwriting the buyer, not the supplier. That means we can support your small and mid-sized suppliers that wouldn’t qualify for traditional bank financing. As a result, you can offer instant working capital to most of your supplier base, not just the biggest accounts. And since our onboarding, credit assessment and funding are all automated, you can extend financing to hundreds of suppliers if necessary.

Your suppliers also get flexibility. They can choose which invoices to finance, whether that’s one invoice per month or all of their volume.

We also support over 100+ countries and multiple currencies, including GBP, EUR, CHF, and USD. As you expand into new markets, you don’t need to onboard a new financing provider each time. Aria scales with you.

Gain non-recourse protection with transparency and control

Like all non-recourse factoring providers, Aria takes on the credit risk. Our risk analysis system combines buyer credit scoring, a fraud detection engine, and invoice validation to reduce the risk of defaults. And it works: our default rate sits at just 0.1%.

In the meantime, you maintain transparency and control over how we operate within your marketplace.

For example, you have flexibility in how invoice validation is handled:

- If invoices are already validated on your platform, you can use our invoice validation endpoint to confirm that.

- If you have a debtor interface but no validation flow, you can embed our invoice validation widget.

- If your product doesn’t include buyer interaction, we can handle validation directly by emailing the buyer.

What’s more, non-recourse isn’t the only option. Some of our partners choose to mix non-recourse and recourse financing on a per-invoice basis. This usually happens when our clients have strong financials and established buyer relationships – at that stage, they feel confident to take on the risk of non-payment in exchange for higher credit limits.

The same flexibility applies to collections. You can collaborate with us to design a recovery workflow that fits your brand and user relationships. When recovery is needed, we lead with dialogue, tact, and professionalism, protecting your reputation while removing operational burden.

You also have control over how fees are handled: you can either absorb them into your pricing or pass them on to your suppliers. It’s up to you.

Embed invoice financing that fits your platform, not the other way around

Unlike rigid plug-and-play solutions, Aria adapts to your business. Think of us as a B2B financing toolkit you can mould to your product, workflows, and tech stack.

Aria’s REST API integrates directly into your existing systems, making it easy to automate financing even if you process high volumes of small invoices. As long as we receive invoice data, we can be embedded wherever it makes sense: within your marketplace, POS, ERP, CRM, or other tools. Plus, there are no channel limitations – in-store, online, or offline sales are all supported.

User experiences are fully customisable. Buyers and sellers go through white-labeled, branded onboarding flows, so they stay within your ecosystem rather than being pushed to a third party. That reduces friction and helps prevent disintermediation.

You’re free to get started with Aria’s manual dashboard before moving to full API integration when you’re ready. Along the way, you’ll have hands-on support from a dedicated implementation manager, a key account manager, and direct access to Aria’s product and finance teams for any questions or feature requests.

How Aria replaced 20 factoring partners with one unified solution for Job&Talent

Job&Talent is an AI-powered workforce platform connecting skilled professionals with companies in essential industries. In 2024 alone, they placed 300,000 workers and handled €1.8 billion in transactions.

Like many marketplaces, it faced a familiar problem: buyers wanted to pay late, while suppliers needed cash immediately. Before Aria, Job&Talent relied on 20 different factoring partners, which was a logistical headache. Multiple systems, manual uploads, and repetitive processes made operations slow and error-prone.

Aria changed that. Integrating seamlessly with NetSuite, Job&Talent invoices now transfer automatically to Aria, and suppliers are able to receive funds in less than 24 hours. What once required three people managing invoices across multiple partners now takes one person and a third of the time.

Read the full case study: From 20 factoring partners to one: How Job&Talent automated invoice financing across Europe

Pay suppliers faster without taking on risk with embedded non-recourse invoice factoring

When suppliers have to wait months to get paid, their growth stalls, which limits what your marketplace can achieve.

Embedded, non-recourse invoice financing changes that. Sellers get paid instantly, your platform stays risk-free, and collections and credit management are handled for you.

With Aria, for example, you can embed non-recourse invoice financing directly into your marketplace and offer faster payouts as a white-labelled feature. This integrated setup improves your users’ experience without adding operational complexity or shifting risk onto your business.

To learn how we can help you scale your marketplace through faster supplier payouts, request a free demo today.

FAQs: Non-recourse invoice factoring

What’s the difference between recourse and non-recourse factoring?

Recourse and non-recourse factoring differ mainly in who bears the risk if a buyer doesn’t pay. In recourse factoring, the invoice issuer is responsible for unpaid invoices, meaning they must repay the factor if a buyer defaults.

Non-recourse factoring, on the other hand, shifts that credit risk to the factoring provider and protects the seller from losses due to buyer insolvency. Non-recourse agreements usually cover buyer bankruptcy within a defined period, but not disputes or late payments caused by product or service issues.

What are the main benefits of non-recourse factoring?

Non-recourse factoring provides faster access to immediate cash while protecting sellers and marketplaces from buyer credit risk. Other benefits include quicker invoice payment, reduced operational burden since the factor handles collections, and overall smoother cash flow. The trade-off of this financing option is slightly higher fees compared with recourse factoring.

Can non-recourse factoring be embedded into my B2B marketplace?

Yes, modern non-recourse solutions like Aria can be integrated directly into your marketplace or platform. This means sellers can request early payment without leaving your interface, and buyers can stick to their preferred payment terms and methods. Embedded solutions can also be white-labelled, which keeps the experience under your brand.

Who are some non-recourse factoring providers in the UK?

Providers offering non-recourse invoice factoring in the UK include Aria, Bibby Financial Services and Close Brothers Invoice Finance. It is sometimes referred to as Bad Debt Protection. Note that each provider has different credit risk coverage, integration capabilities, fees, and eligibility requirements, so be sure to evaluate them carefully based on your business needs.