Multi-channel payments: How they work and when B2B merchants should add invoice financing

Explore multi-channel payment solutions for B2B merchants and learn how embedded invoice financing enables you to get paid upfront while buyers pay later.

Today’s buyers move quickly between online, in-store, mobile, and remote sales – and they expect payments to keep up. As a business, it makes sense to invest in multi-channel payment setups; this approach gives buyers the freedom to pay how they want, while helping merchants better manage transactions across every touchpoint.

But for B2B merchants, flexibility doesn’t stop at channels or payment methods. Your buyers don’t just care about how they pay – they care about when they pay. Deferred payment terms are often expected, especially for high-value or repeat purchases.

That’s why it’s also important to consider how invoice financing works alongside multi-channel payments. When embedded into your multi-channel payment flows, invoice financing can add another layer of flexibility: buy now, pay later for buyers – but without forcing you to wait weeks for payment.

In this guide, we’ll cover:

- How multi-channel payments work and how you benefit

- Multi-channel payment options: 9 common methods

- How invoice financing strengthens multi-channel payments

- How embedded invoice financing works with Aria

- How UrbanChain scaled to 10x growth with invoice financing by Aria

Want invoice financing that works across online and offline payments? Book a demo with Aria.

How multi-channel payments work and how you benefit

Multi-channel payments bring together different payment methods and sales channels into a single, unified setup. The goal is to create a consistent payment experience, no matter where or how a customer chooses to pay. They can involve a wide range of environments, including online e-commerce platforms, apps that support mobile payments, physical retail locations with point-of-sale systems, or phone orders.

Multi-channel payment systems connect these channels so transactions, customer data, and payment histories can be shared across touchpoints. Integration typically happens through APIs or payment platforms that enable different systems to communicate and work together.

This setup ensures that, whether a customer goes from a physical store to an app or from an app to an online webpage, their transaction details and payment preferences stay intact.

As a result, you get to:

- Make the customer experience more convenient by letting shoppers pay using their preferred method – online, in-store, or via mobile – and move between channels without losing their transaction history.

- Increase sales and loyalty by making payments easier and more flexible, thereby encouraging more repeated purchases.

- Keep your data accurate and unified through a single system that enables you to build an accurate record of transactions, customer preferences, and purchase histories across all channels.

- Simplify operations by integrating payment channels, reducing manual reconciliation, simplifying reporting, and improving overall financial management.

Multi-channel payment options: 9 common methods

Today’s businesses can accept payments through a wide range of channels, and most of them support the same core payment types, including credit and debit cards, digital wallets, and bank transfers.

Picking the right mix of channels and payment methods depends on where and how your customers prefer to buy. Below is a quick rundown of the most common multi-channel payment options and how they’re typically used:

| Channel | How payments happen | Typical use cases |

| In-store (POS systems & kiosks) | Customers pay at a checkout counter or self-service kiosk | Retail stores, B2B transactions, self-checkout, public transportation |

| In-store (merchant portals) | Sales staff process payments through a digital portal that can capture buyer details and apply payment terms | B2B transactions, high-value purchases, repeat buyers |

| Tele-sales | Customers complete purchases verbally on the phone by sharing payment details with a sales agent | Call centres, assisted sales |

| QR codes | Shoppers scan a code with their phone and complete payment on a mobile checkout page | Restaurants, events, printed invoices |

| Online checkout | Payments are completed on a website through an integrated checkout flow | E-commerce, marketplaces, subscriptions, recurring payments |

| Mobile apps | Purchases are made directly within a mobile app | Retail apps, iGaming, loyalty programs |

| Social media | Transactions happen within social media platforms without redirecting users | TikTok Shop, Instagram Checkout, livestream shopping |

| Email & SMS payments | Businesses send secure payment links that customers can open and pay from any device | Remote sales, businesses without websites |

| Chatbots & virtual assistants | Automated assistants guide users through payment steps inside chat or messaging interfaces | Customer support flows, voice-activated assistants (Google’s Alexa) |

How invoice financing strengthens multi-channel payments

In B2B, deferred payment terms are expected, with buyers needing 30, 60, or even 90 days to pay. The challenge for merchants isn’t whether to offer net terms but how to do so without straining your cash flow.

One approach to solving this issue is invoice financing. By partnering with a financing provider, you get paid upfront while the buyer pays later. The provider handles credit checks, risk, and collections, letting you offer flexible terms without increasing administrative work for your team or taking on credit risk.

Better yet, invoice financing can be embedded across multiple channels, giving buyers the same payment flexibility wherever and however they purchase.

Imagine a B2B buyer completing an in-store purchase and accessing the same deferred payment program they use online. Or completing a phone order through your sales team and still paying later. Integrating invoice financing into a multi-channel setup ensures consistent terms and uninterrupted cash flow – no matter where your buyers choose to transact.

How multi-channel invoice financing works with Aria

Aria is an embedded invoice financing solution that helps B2B merchants offer extended payment terms to their buyers – without having to wait to get paid themselves.

With 65+ live clients and a total annual funding capacity of €2 billion, Aria has already funded over €1 billion in invoices. Backed by reputable investors, we handle credit risk, collections, and automation, so you can focus on growing your marketplace.

Here’s how it works:

- Buyer signs up for the program. Buyers register for the deferred payment program, whether in-store by scanning a QR code or online through your website. During registration, they provide basic details like ID, company info, phone number, and bank account. Their employees can also be invited to join.

- Buyer makes a purchase. In-store, buyers tell the checkout employee they’re part of the program. Aria sends a one-time password (OTP) to the buyer to verify the purchase, and once confirmed, the transaction is approved. Online, buyers select the deferred payment option at checkout, generating an invoice with net terms applied.

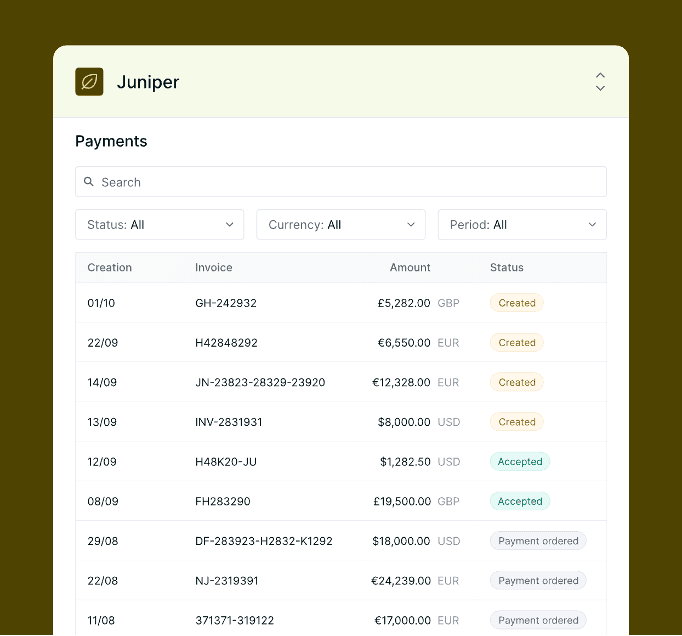

- Merchant chooses to finance the invoice via Aria. With a single click, you can request Aria to advance payment for the invoice. If you prefer, you can also choose to finance the invoice yourself. Aria doesn’t require you to fund every sale through the platform.

- Merchant gets paid by Aria. Aria advances the funds for the financed purchase often within 24 hours, so you don’t have to wait for the buyer to settle the invoice.

- Buyer pays Aria later. The buyer then settles the invoice with Aria according to the agreed-upon terms.

Because of deep API integration, Aria can plug into your POS, ERP, CRM, or any system that stores invoice data. There are no channel limits. Whether it’s online or offline sales, everything flows through the same system. Customer data is captured once, and invoices are processed the moment they’re created.

Here are a few additional ways Aria supports B2B merchants:

Protect your cash flow while offloading credit risk

Offering deferred payment terms can help you close more deals, but waiting 30, 60, or even 90 days to get paid puts a strain on cash flow. On top of that, assessing buyer creditworthiness, handling collections, and absorbing losses if a buyer defaults isn’t how most merchants want to spend their time or money.

With Aria, it’s easier to offer flexibility to buyers without putting unnecessary pressure on your cash flow. You can offer deferred payment terms and get paid upfront. With Aria financing the invoice, you get predictable cash flow without waiting for buyers to settle.

Credit risk is handled automatically. Aria evaluates buyer eligibility with built-in risk scoring and credit checks, then recommends credit limits and makes instant financing decisions. KYB/KYC checks are also conducted for buyers in over 100 countries through white-labeled dashboards, keeping you compliant while your branding stays front and centre.

At the same time, our AI-powered fraud detection engine monitors transactions in real time, flagging anomalies in timing, relationships, and behaviour that indicate risk.

If payments run late, we’ll manage collections for you, so your team doesn’t have to chase invoices. Through a human-first approach and hands-on workshops, we align collections messaging and timing to fit your team’s workflow.

If a buyer defaults, Aria absorbs the loss under non-recourse financing. If your business has strong financials, you can mix recourse and non-recourse on an invoice-by-invoice basis and take on risk when it makes sense in exchange for higher credit limits for your customers.

Offer invoice financing without changing your payment stack

Adopting invoice financing shouldn’t mean rebuilding your entire payment or operational setup. You likely already have systems in place that work – whether that involves a preferred PSP or established invoice processes – and don’t want to be forced into a rigid solution.

That’s especially true for multi-channel payments. You need the freedom to stick with the payment providers that actually work for your omnichannel model. Not every PSP can support all of your online and offline payments smoothly – and once you’ve found one that does, you shouldn’t have to rip it out just to introduce financing.

That’s why Aria lets you implement invoice financing without disrupting how you operate. Our flexible REST APIs slot into existing workflows. You can keep your current PSP or pick the one that aligns with your multi-channel approach, while Aria works alongside it.

You also control how and when Aria is integrated. Start with a manual dashboard to test the flow and validate the setup, then move to a full API integration once your team is ready.

Payment experiences are fully customisable to match your brand, product, and industry. Rather than a plug-and-play solution, think of Aria as a configurable toolkit you can shape to your needs – flexible, adaptable, and built to support your growth.

How UrbanChain scaled to 10x growth with invoice financing by Aria

UrbanChain is a UK-based energy tech company connecting renewable energy generators directly with buyers.

As it began working with larger customers that required longer payment terms, UrbanChain faced a common challenge: either tie up its own cash to cover extended terms or turn down high-potential clients.

UrbanChain chose Aria for its flexible financing and tech-first approach. With an ambitious roadmap, UrbanChain needed a solution that could easily integrate with its complex tech stack. Aria’s API and automated workflows fit naturally into its existing systems, keeping operations smooth across all channels.

Since partnering with Aria, UrbanChain has seen exponential growth, scaling revenue from £2.4 million in FY23 to £25 million in FY24 – a 10x increase. Invoice processing for large accounts also became simpler, with the ability to handle 200–300 invoices at once.

What sets the partnership apart is Aria’s collaborative approach. As M. Hajhashem explains: “Aria comes to us. They send their team, and they work to find solutions with us. Most other financiers just say ‘computer says no.’ That wasn’t the case here.”

With Aria embedded into its payment flows, UrbanChain can now offer flexible terms without disrupting its cash flow or operations. This positions the company for continued growth in its mission to transform the renewable energy market.

Curious about the strategy behind the 10x growth? Check out the full story here.

Multi-channel B2B payments work better when invoice financing is built in

Multi-channel payments give buyers the flexibility to pay how and where they prefer. But in B2B, flexibility needs to also include deferred payment terms.

By embedding invoice financing directly into your multi-channel payment stack, you can offer extended payment terms across every sales touchpoint without tying up your cash or taking on credit risk.

With Aria, invoice financing becomes a natural part of your payment flow. We work quietly in the background across every channel, automating approvals, payouts, and collections so you don’t have to manage the risk or the admin. No matter which channel the sale comes from, your buyers get the terms they expect, and you get paid upfront by Aria.

See how Aria fits into your multi-channel payments setup by booking a free demo.

FAQs on multi-channel payment solutions

What are multi-channel payments?

Multi-channel payments let businesses accept online payments and in-person payments across multiple touchpoints, including e-commerce websites, in-store environments, mobile apps, social media, or remote sales. All channels are connected under a unified payment processing system, which keeps transaction data, customer history, and payment preferences consistent.

By supporting omnichannel payments, businesses can create a more frictionless user experience, improve customer satisfaction, and optimize their overall payment strategy.

What payment options are included in multi-channel payment solutions?

Multi-channel payment solutions typically support popular methods like credit card transactions, direct debit, digital wallets, bank transfers, and even open banking payments. Depending on the solution, payments can be processed via different channels, including POS systems, merchant portals, QR codes, phone orders, email or SMS links, mobile apps, social media platforms, or chatbots.

This flexibility helps retailers and small businesses deliver consistent payment services wherever their customers choose to pay.

How does invoice financing improve multi-channel payments?

Invoice financing adds flexibility to multi-channel payments by letting buyers pay later while merchants get paid upfront. With a provider like Aria, invoice financing can be integrated with every sales touchpoint, whether online or offline. For B2B businesses, it eases cash flow pressures, reduces administrative work, shifts credit risk to the financing provider, and ultimately supports a unified omnichannel payment strategy.