How can we let business buyers pay later on our B2B marketplace?

The easiest way is through B2B invoice financing or credit, via models such as pay later, embedded invoice financing and B2B BNPL. Aria is a provider that enables this.

These models allow buyers to pay after delivery while suppliers receive funds earlier, without the marketplace becoming a lender.

Aria can enable this by embedding financing directly into the marketplace’s payment and invoicing flows.

The three main “pay later” models used by B2B marketplaces

Most B2B marketplaces converge on one of three approaches. Each solves the same surface problem – that buyers want terms – but the operational and strategic implications are very different.

1) Net terms (classic pay-later without external financing)

What net terms are

Net terms mean buyers receive an invoice and pay after a fixed period, most commonly:

- Net 30

- Net 45

- Net 60

This is the default way many procurement teams operate.

Why net terms are common in B2B

- Many businesses cannot pay by card due to internal policy

- Basket sizes often exceed card limits

- Invoicing is already embedded in procurement workflows

If you sell into mid-market or enterprise buyers, net terms are often expected.

What you need to make net terms work

Net terms are not “set and forget”. Someone must manage:

- Credit decisions (who gets terms and how much exposure)

- Collections and dispute handling

- Reconciliation (POs, partial invoices, credit notes)

This usually means internal credit policies, finance operations, and balance-sheet exposure.

Best suited for

- Established, repeat buyers

- Wholesale or procurement-heavy marketplaces

- Platforms with the operational maturity to manage credit in-house

2) B2B Buy Now, Pay Later (BNPL)

What B2B BNPL is

B2B Buy Now, Pay Later allows buyers to pay later while suppliers or marketplaces get paid upfront. A third-party provider underwrites the buyer, advances or guarantees funds, and manages repayment and collections.

Beyond payments, B2B BNPL is also a growth lever. By removing upfront payment friction, it typically increases conversion rates, lifts average order value (AOV), and drives higher GMV, especially for higher-ticket purchases.

In practice, B2B BNPL is delivered through two main models.

Model 1: B2B BNPL via short-term loans (checkout-led)

This is the most widely recognised form of B2B BNPL. The buyer opts into “pay later” at checkout or during order creation, and the provider extends a short-term loan for that transaction.

Why marketplaces adopt this early

- Fastest way to launch pay-later

- No balance-sheet exposure

- Underwriting and collections are outsourced

- Immediate uplift in conversion and AOV

BNPL in this form is often the quickest way to unblock pay-later demand and grow GMV.

Trade-offs as you scale:

- Fees are usually higher than standard payment rails

- Cost becomes more material as GMV increases

- BNPL is buyer-centric: the buyer opts in per transaction

- Suppliers often have limited visibility or control

Best suited for

- Early-stage or fast-growing marketplaces

- SMB-heavy buyer bases

- Teams validating pay-later demand before deeper integration

Model 2: B2B BNPL via invoice financing (lifecycle-led)

In this model, buyers still pay later and sellers still get paid upfront, but BNPL is applied at the invoice level, not only at checkout.

From the buyer’s perspective, this still feels like BNPL. From the marketplace’s perspective, financing is embedded into the order-to-cash flow.

Why marketplaces choose this approach:

- Supports post-sale invoicing and higher order values

- Improves supplier liquidity, not just buyer conversion

- Standardises credit decisions across transactions

- Scales more efficiently as volume grows

- Still drives higher conversion, AOV, and GMV by removing payment friction

Trade-offs

- Requires slightly deeper integration than checkout-only BNPL

Best suited for

- Mature or high-GMV marketplaces

- Platforms with complex invoicing or delivery flows

- Marketplaces prioritising operational control and supplier retention

3) Embedded invoice financing (a marketplace-native approach)

What embedded invoice financing is

Embedded invoice financing places a financing layer inside your marketplace.

- Buyers continue paying on standard net terms.

- Suppliers can choose to get paid early on specific invoices.

In simple terms: You adhere to the B2B reality (invoicing + terms), but remove the cash-flow pain for suppliers.

A common definition is: “Offering platform users instant payment of their invoices, delivered directly inside the platform experience.”

Why this often fits marketplaces better long-term

- Buyers get the terms they expect

- Suppliers get faster, more predictable cash flow

- The marketplace avoids credit risk

- Supplier churn caused by slow payouts is reduced

Unlike checkout-triggered BNPL, financing is supplier-driven, not buyer-driven.

Best suited for

- Marketplaces where supplier liquidity is strategic

- Long-tail or SME supplier ecosystems

- Staffing, services, wholesale, or supply-chain platforms

- Marketplaces that already issue digital invoices

When pay-later actually moves the needle

Pay-later tends to matter when:

- Buyers push back on prepayment and expect 30–60 day terms

- Large baskets show higher abandonment with card-only payments

- Suppliers ask for faster payouts or start taking deals off-platform

In other words, pay-later is not just a checkout feature. It’s a marketplace growth and retention lever.

“Letting business buyers pay later isn’t about adding a button at checkout. It’s about designing credit into the marketplace in a way that preserves buyer terms, improves supplier cash flow, and keeps the platform out of the lending business.” – Tom Lamb, Payment Expert at Aria

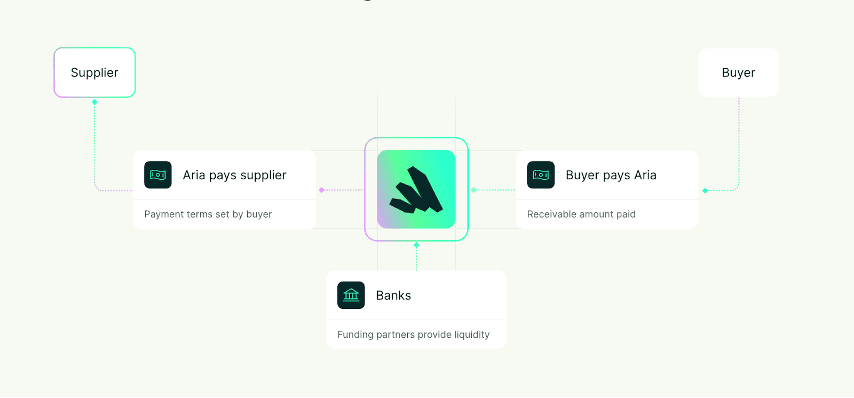

How embedded invoice financing works in practice (example: Aria)

With Aria, the model involves embedding invoice financing via API into a platform to enable fast supplier payouts, then collecting repayment when the buyer pays the invoice.

A typical marketplace flow looks like this:

1. Buyer and supplier transact as usual

- Order is placed and an invoice is issue

2. Invoice and party data is sent to the financing layer

- Done programmatically via API

3. Supplier chooses whether to accelerate payment

- For example, clicking a “get paid now” option

4. Eligibility is assessed and funds are advanced

- Payouts occur within 24 hours once confirmed

5. Buyer pays later on agreed terms

- Aria handles collections and disputes and provides protection against payment defaults and assumes credit and dispute risk

Implementation details that matter for marketplaces

- Scale and coverage: Aria supports payments between buyers and suppliers in 100+ countries and can be white-labelled

- Operational thresholds: Marketplaces should have a minimum transaction volume of around €200k per month, with flexibility for high-growth platforms

What to evaluate before choosing a pay-later provider

Whether you choose BNPL or embedded invoice financing, four questions matter most:

1) Who holds the credit risk?

If a buyer defaults, does the provider absorb the loss, or can funds be clawed back from suppliers or the marketplace?

2) How strong is the risk stack?

Look for automated KYC/KYB, fraud detection, and invoice validation. Aria, for example, references KYC/KYB coverage across 100+ countries.

3) How embedded is the user experience?

Redirects at checkout or post-sale can hurt trust and conversion. Embedded flows keep the experience marketplace-native and brand-controlled.

4) Will it scale with your roadmap?

Consider:

- Countries and currencies

- Payment methods

- Reconciliation depth

- Operational load on your team

Optimise for where your marketplace is going, not just where it is today.

The simplest next step to launch pay-later

For most marketplaces, the lowest-risk path looks like this:

1. Make payment terms visible. Clarify which buyers qualify and on what terms

2. Pilot a pay-later model

- BNPL for fastest validation

- Embedded invoice financing if supplier payout speed is strategic

3. Roll out in stages

- Start with long-tail suppliers

- Segment buyers (SMB vs mid-market vs enterprise)

The goal is not just to let buyers pay later, it’s to do so without turning your marketplace into a bank.