B2B e-commerce payments for marketplaces: what to offer buyers and suppliers

Discover which B2B e-commerce payment methods marketplaces can implement and learn how invoice financing can bridge the payment gap between buyers and sellers.

The right B2B e-commerce payments setup in a marketplace determines whether users are getting paid in full and on time – and this can directly impact their cash flow, growth, and trust in your platform.

But what’s the “best” payment option?

For a typical B2B seller, the answer is usually simple: whatever makes it easiest for buyers to pay. That might mean credit cards for speed, bank transfers for larger invoices, or Buy Now, Pay Later (BNPL) methods that give buyers more flexible payment options.

For B2B marketplaces, the question gets a bit more complicated.

This is because you’re not just optimising for one customer. You’re designing a payment experience that has to work for two sides at once. Buyers want flexible payment terms, while your sellers want to get paid quickly and reliably. And that leaves you stuck in the middle, trying to satisfy both without tying up your own capital or taking on unnecessary risk.

In this article, we’ll break down:

- The most common B2B e-commerce payment methods

- How financing can bridge the payment gap between buyers & sellers (and two of the most popular methods)

- How embedded invoice financing works with Aria

- Why B2B marketplaces choose Aria as their invoice financing partner

- Case study: How Aria supported Malt’s international expansion to 40+ countries

Aria is an embedded invoice financing solution for B2B marketplaces. Find out how we can make invoice financing fit your flow and use cases with a free demo.

The most common B2B e-commerce payment methods

As a marketplace, you ideally want to design a B2B payment setup that works for both buyers and sellers. This means you’re not just choosing how money moves – you’re choosing when.

Let’s break down the most common options for B2B e-commerce payments, starting with payment timing and then the payment methods themselves.

What are your options for payment timing?

When buyers pay and when sellers get paid can make or break adoption on both sides. Here are the most common timing models you’ll see in B2B e-commerce:

| Payment option | How it works | Buyers | Sellers |

| Invoice payments | Buyers receive the goods or services first and pay later, usually within 30, 60, or 90 days. | Enjoy more breathing room and better cash flow. | May face delayed payouts and the risk of late or missed payments. |

| Instalment plans | The total cost is split into scheduled payments over time. | Can afford higher-value purchases more easily. | May see higher order values, but payments arrive gradually and require ongoing management. There’s also a risk of late or missed payments. |

| Cash on Delivery (COD) | Payment is made at the moment goods are delivered to the buyer. | Can inspect items before paying. | Risk refused deliveries and delayed cash flow, though they may reach a wider audience. |

| Prepayment | Buyers pay upfront before delivery or service begins. | Take on more risk and tie up cash upfront, which is why this model can be a tough ask for buyers in larger B2B deals. | Get immediate, guaranteed payment. |

What are the most popular B2B payment methods?

Once timing is set, the next decision is how the money moves between buyers and sellers:

| Payment method | How it works | Buyers | Sellers |

| Bank transfers | Buyers manually send funds from their bank account to the seller’s account. | Can pay using a secure, familiar option, but it can be inconvenient for frequent or cross-border online payments. | Benefit from low fees, though settlement can be slow, especially for international transfers. |

| Direct Debit | Seller pulls funds directly from the buyer’s bank account on a scheduled basis. | Enjoy convenience, but have less control over timing and risk overdrafts. | Get predictable, recurring revenue with low transaction fees. |

| Credit cards | Buyers pay by credit card and settle later with their card provider. | Enjoy speed, convenience, and sometimes rewards – but risk high interest if balances aren’t paid. | Receive funds quickly, but pay higher fees and face chargeback risk since buyers can dispute transactions with their provider and reverse the payment. |

| Debit cards | Buyers pay by debit card, and funds are taken from the buyer’s bank account via card networks at checkout. | Avoid the risk of accumulating interest, but need sufficient funds immediately. | Receive fast payments but still face potential chargebacks and disputes, especially if a buyer claims a transaction was unauthorised. |

| Cheques | Buyers write and send a paper cheque that the seller deposits into their own account. | Typically only use cheques when digital payment options aren’t available. This method involves slow processing, manual work, and poor visibility into payment status. | Deal with slow processing, bounced checks, and manual reconciliation. |

| Trade accounts | Transactions accumulate over a fixed period (usually monthly) and are settled at the end of the period. | Simplify their payment flows and decrease operational workload, but usually require credit approval and need to maintain strict payment discipline. | Encourage repeat purchases and larger orders, but take on some credit risk and delay cash collection until the specified date. |

How financing can bridge the payment gap between buyers and sellers (and two of the most popular methods to enable this)

It can be hard to pick the “right” payment setup because of the mismatch in the demands of buyers and sellers: most buyers prefer to pay on extended terms, while sellers want predictable revenue – ideally in near real time.

That tension puts marketplaces in a tough spot, which is where financing comes in.

Instead of forcing one side to compromise, a third-party financing company can front the money to sellers while letting buyers pay on terms that work for them. In most cases, the company also handles collections and takes on the risk of non-payment.

Note that financing doesn’t replace your payment methods. It sits alongside them. Buyers can still pay via bank transfer, card, or other options. Financing just changes the payment flow: who pays whom and when.

There are two popular approaches:

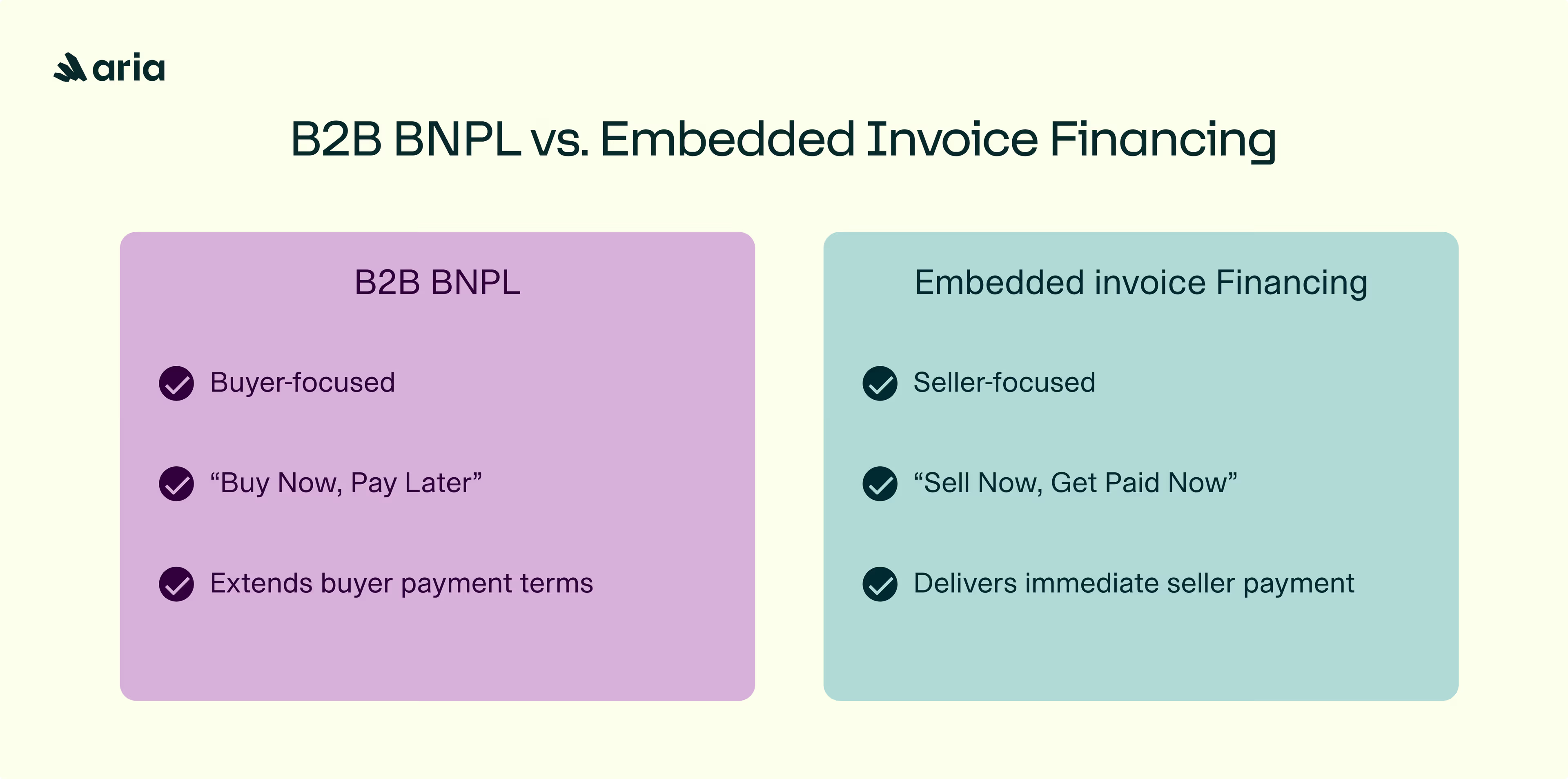

1. Buy Now, Pay Later (BNPL): A common buyer-centric option

B2B BNPL is a buyer-driven option many people recognise. Here’s how it works:

- The buyer selects BNPL at checkout.

- A third-party BNPL provider pays the seller.

- The buyer repays the BNPL provider over time, sometimes in instalments.

For buyers, this means more flexibility and less upfront pressure. For sellers and marketplaces, it means you don’t have to take on credit risk or manage collections.

The downside is that BNPL is inherently buyer-centric: sellers only access faster payments when the buyer actively opts in by choosing BNPL as their preferred payment method at checkout. As a result, sellers’ cash flow is closely tied to buyer behaviour and therefore out of their control.

2. Invoice financing: A seller-focused solution that works for both sides

Invoice financing is designed to satisfy both the seller and the buyer. Here’s how it typically goes:

- The seller issues an invoice to the buyer as usual.

- The seller passes (effectively sells) the invoice to a financing provider.

- The provider advances the payment to the seller (often minus a small fee).

- The buyer pays the invoice, per the original terms, directly to the financing provider.

For buyers, very little changes other than the fact that their payment now goes to the financing provider instead of the seller. They still get the net terms they expect and can use their preferred payment methods.

Sellers, on the other hand, experience a clear shift in cash flow and risk. They can choose to get paid right away and no longer wait weeks for funds to come in. Plus, the risk of late or missed payments is transferred to the financing provider.

This is why invoice financing is especially valuable for marketplaces. You can satisfy the demands of both sellers and B2B customers, and you don’t have to use your own capital, chase payments, or manage credit risk to do so.

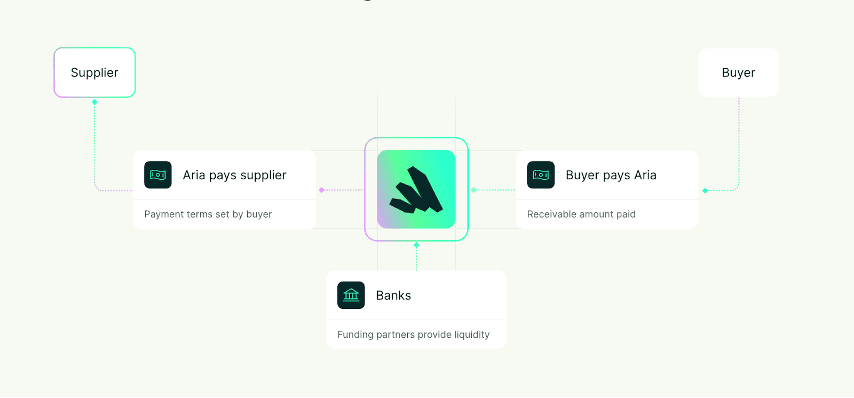

How embedded invoice financing works with Aria

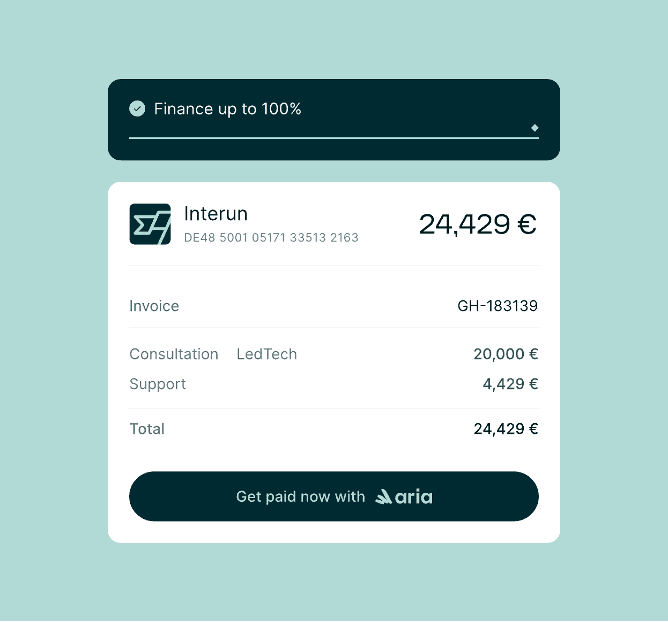

Aria is an embedded invoice financing solution built for B2B marketplaces. With Aria, you can embed invoice financing directly into your platform using our flexible REST APIs. Everything is white-labeled, and your users never leave your marketplace. Sellers sign up and onboard right from your platform. Invoices are sent to buyers as per usual, and buyers can validate them in a few clicks.

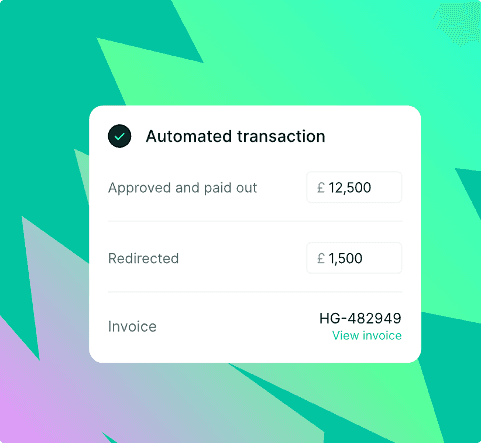

Once an invoice is validated, the seller can request instant payment with a press of a button. Aria advances up to 100% of the invoice, usually within 24 hours. The buyer then pays us on their usual terms – with no disruption to their payment journey.

Why this matters for B2B marketplaces:

- Sellers can request payouts and get them instantly, which builds trust and keeps them active on your platform.

- Buyers pay on their normal terms using their preferred method, so conversion stays high.

- You keep ownership of the user experience without tying up funds, taking on credit risk, or increasing your team’s operational burden.

Why B2B marketplaces choose Aria as their invoice financing partner

With over 500,000 invoices funded across 70+ live clients, Aria supports B2B marketplaces that require robust B2B payment solutions designed around net terms, multiple sellers, and complex payment workflows.

Here’s what we help clients like Job & Talent, Malt, and StaffMe with:

Keep both sellers and buyers engaged through faster payments

B2B buyers are used to longer payment terms – typically 30, 60, or 90 days – which leave sellers waiting for the cash they need to restock and keep up with demand. And if a buyer is late? Sellers end up chasing payments themselves, adding time and stress.

Aria changes that dynamic. Buyers can stick to their usual terms and pay however they prefer. Sellers are given the choice to get paid in 24 hours, regardless of buyer behaviour.

Because we underwrite the buyer, not the seller, we can even serve small, long-tail suppliers that often can’t get bank financing. Our invoice acceptance rate is very high – over 90% of invoices are funded – and our financing is flexible. Users can finance anywhere from one invoice a month to every invoice in their flow.

Once the invoice is funded, we handle the rest. Buyers pay Aria on their regular payment terms. If they’re late, we take care of collections. We’re also insured against non-payment, so you never have to worry about repaying the money we advance.

In the long run, faster payments mean suppliers can handle more transactions – and this grows transaction volume for your marketplace, all without taking on credit risk.

Simplify operations with a single automated API solution that scales with you

While it’s possible to finance sellers yourself, using your own funds quickly strains your cash flow and leaves little to reinvest in growth.

On top of that, financing sellers in-house means juggling a mountain of responsibilities: credit assessments, KYC checks, fraud protection, collections, defaults, insurance, verification of goods and services, and more. You’d likely need multiple vendors for these tasks, making your workflow even more complicated and costly.

As your marketplace grows, it only gets harder. Without the right technology and automation, manual processes start leaving money on the table.

That’s where Aria comes in. We not only have the capacity to finance invoices – up to €2 billion – but we also handle all the heavy lifting behind the scenes. Our technology scales with your marketplace. Dozens of risk checks that used to take days are processed automatically, with 92% instant decisioning. All we need is a company registration ID to determine financing limits and advance funds.

Plus, we support multiple currencies and over 100 countries, so expanding internationally is no problem. With Aria, you get a single, reliable partner that grows as you grow, removes operational friction, and keeps cash flowing smoothly across your marketplace.

Stay in control of the customer experience by embedding financing exactly as you’d like it

No two B2B marketplaces are built the same, from complex payment flows to different fee splits and custom logic for buyers, sellers, and commissions. Even checkouts can look completely different from one platform to the next. This means you’ll want a solution that can fit seamlessly into your existing operations, not one that forces you to rebuild your product just to make things work.

Aria is designed to fit your marketplace – not the other way around. We slot straight into your workflows, whatever your tech stack or industry. The payment experience is fully white-labeled and customised to match your brand and product, from onboarding to payouts.

Think of Aria as a B2B toolkit: we give you the building blocks. You decide how to use them.

All the while, you get hands-on support from day one:

- A dedicated implementation manager

- A key account manager who knows your business

- Direct access to our product and finance teams for more complex or unique needs

You can start small with a manual dashboard, then move to a full API integration when your team is ready. We scale with you, adapting to your product, your pace, and your technical maturity.

Pricing also stays in your control. Our fee structure is flexible, so you can choose what works best for your marketplace:

- Absorb our fee and integrate it into your overall pricing

- Pass the fee on to your suppliers, for example, via a small supplement

How Aria supported Malt’s international expansion to 40+ countries

Malt is a leader in Europe’s freelancing market, helping more than 70,000 companies work with 700,000 independent experts across a wide range of fields. As it grew, Malt faced two major challenges.

First, they needed to bridge the gap between freelancer payments and customer repayments. Freelancers wanted fast access to cash, but clients were still paying on standard terms.

Second, as Malt expanded internationally, they had to manage payments in multiple currencies and new geographies – all while keeping operational overhead low and minimising errors in data entry.

How Aria helped

With a smooth API integration, Malt freelancers can now access rapid payments for their assignments in just a few clicks. Specifically, we’ve helped them enable:

- Fully embedded advance payments within Malt’s existing workflows

- Automated credit assessment, invoice validation, and advanced payment processing

- Multi-currency support for €, £, and $

- Tracking of reimbursements and collections

This automation reduced workload for Malt’s operational teams, cut down on errors, and enabled the platform to handle high volumes of transactions with ease.

Today, Aria supports Malt across 45 countries and has financed more than 50,000 invoices. On average, invoices are financed in under nine hours, giving freelancers fast access to their earnings while Malt continues to grow globally.

Alexandre Fretti, Co-CEO of Malt, describes the partnership: “The challenge for a player like Malt is to find partners who evolve at the same speed as us. We are confident that Aria will have the capability to support us on a global scale.”

Reduce friction in B2B e-commerce payments with embedded invoice financing

Buyers want flexibility. Sellers need fast, predictable access to funds. Embedded invoice financing solves this tension: sellers get instant, guaranteed payments, while buyers continue paying on their preferred terms.

Immediate payouts mean sellers can reinvest in inventory or expand services. Of course, more active sellers contribute to a more thriving marketplace – and faster growth for your platform.

By embedding a financing solution like Aria directly into your marketplace, you get to reduce friction in B2B e-commerce payments, minimise operational headaches, and keep your UX intact.

Discover how we can help you with a free demo.

FAQs: B2B e-commerce payments

What are the most common B2B e-commerce payment methods?

Common B2B e-commerce payment methods include bank transfers, direct debit, credit cards, debit cards, and checks, with timing options like invoice (Net 30/60/90), installments, prepayment, or cash on delivery.

How do e-commerce payments work on a B2B marketplace platform?

On a B2B marketplace platform, e-commerce payments are more complex than in standard B2B or B2C scenarios because you’re managing two sides at once. Typically, buyers pay using their preferred method, while sellers wait for funds based on agreed terms. Marketplaces can integrate embedded financing to advance payments to sellers, maintain buyer flexibility, and streamline overall B2B payment operations.

What is the best B2B e-commerce payment solution for marketplaces?

The best B2B e-commerce payment solution for marketplaces balances flexibility for buyers with fast, predictable cash flow for sellers. Embedded invoice financing solutions, such as Aria, are increasingly popular because they integrate directly into the marketplace. Sellers can receive instant payments on invoices, buyers stick to their preferred payment methods, and the platform avoids operational headaches, credit risk, or cash strain.