B2B Buy Now, Pay Later (BNPL): How It Works and Its Benefits

Learn how B2B BNPL works for marketplaces, when it’s the right fit, its limitations, and how alternative financing models can better support buyers and suppliers.

If you’re a B2B marketplace, you’re facing a constant tension: buyers want to pay on their own later payment terms, but your suppliers want to be paid right away. And while financing that gap yourself might work at first, it quickly ties up your working capital and slows down scaling.

That’s why more and more platforms are looking at B2B Buy Now Pay Later (BNPL). With this approach, a third-party BNPL provider offers extended payment terms to buyers, without you having to put your own capital at risk. They also handle credit checks and collect repayments, taking a lot of operational load off your team.

In this guide, we’ll help you understand whether implementing B2B BNPL is the right choice for your marketplace. We’ll also show you how embedded invoice financing can help you offer regular payment terms to buyers while also offering same-day payouts to suppliers – and why this may be more beneficial as a marketplace.

We’ll cover:

- How does B2B BNPL work?

- When it makes sense to implement B2B BNPL for your marketplace

- Why B2B BNPL may not always be the right choice for your marketplace

- Why B2B marketplaces are turning to embedded invoice financing solutions like Aria

- Why choose Aria as your embedded invoice financing partner

Aria is an embedded invoice financing platform that helps B2B marketplaces offer faster payouts to suppliers – without tying up their own funds. Speak to one of our financing experts to find out how we can help you.

How does B2B BNPL work?

Just like consumer BNPL, B2B “Buy Now Pay Later” lets business buyers receive the products or services they buy right away and pay for them on deferred payment terms – typically 30, 60, or 90 days later – without incurring interest charges.

In a B2B marketplace, BNPL can be embedded right into the checkout flow and experience, allowing the buyer to choose at the point of purchase whether they want to pay now or later. The B2B BNPL provider takes care of credit checks, underwriting, and collections, while the marketplace simply facilitates the transaction by offering BNPL as a payment method.

Here’s a step-by-step example of how B2B BNPL works during a transaction at a marketplace:

- The buyer selects goods or services from a supplier. At checkout, they choose a “Buy Now, Pay Later” option (such as “Pay in 60 days” or “Split into 3 payment installments”) that’s powered and branded by the BNPL provider.

- The buyer is redirected to the BNPL provider’s flow.

- The BNPL provider runs a real-time credit check.

- If approved, the buyer completes the purchase on deferred payment terms.

- Once the B2B transaction is confirmed, the BNPL provider pays the supplier according to the agreed payout schedule.

- The supplier ships the goods or offers the services as usual.

- The buyer receives the product and services.

- The buyer pays back the BNPL provider according to the agreed schedule. The marketplace is generally not involved in the post-purchase repayment process.

When it makes sense to implement B2B BNPL for your marketplace

It usually makes sense to implement B2B BNPL when you’ve reached a certain volume of transactions per month and when many of your buyers are demanding to pay with later terms.

Depending on the size of your buyers’ companies, they may need to adhere to company payment terms and they can’t use credit cards as these are for smaller amounts.

Without the ability to pay on their own payment terms, they may switch to a different marketplace that allows them to pay at 30, 60 or 90 day terms. And because buyers can purchase goods and services right away without actually spending funds there and then, they might place high-value orders more often.

All of this boosts your transaction volume and improves conversion rates.

However, B2B BNPL isn’t always the answer if you also want to solve supplier cash flow and fast payouts. In fact, there are other forms of third party financing that can be a much better fit for your marketplace, such as embedded invoice financing.

Why B2B BNPL may not always be the right choice for your marketplace

Although BNPL can be a good way to solve a short term problem, as a marketplace, you may face issues at the time of scaling and retaining suppliers.

This is for a number of reasons:

1. BNPL is buyer-centric, leaving suppliers with less control

One of the biggest challenges marketplaces face is supplier cash flow. Suppliers want to be paid quickly – slow payments limit how much they can sell. Because many small suppliers struggle to access bank financing and often rely solely on marketplaces, they have few alternatives. As a result, they’re more likely to switch to a platform that offers faster payouts. This is an issue that BNPL doesn’t solve.

That’s because most BNPL products are built around buyer behaviour. Once a buyer selects BNPL at checkout, the entire financing process shifts into the provider’s hands: they run the credit checks, set repayment terms, manage communication, and handle collections.

As for the supplier, they simply get paid, but they don’t get a say in when financing is triggered – it’s up to the buyer to select BNPL at checkout when they need it.

Plus, suppliers rarely get to see whether a buyer defaults or if any disputes are taking place.

In B2B ecommerce, where long-term and high-value buyer-seller relationships matter, this lack of insight can leave suppliers feeling disconnected. They’re put in a passive role that simply doesn’t match how B2B relationships actually work.

For marketplaces that rely on active sellers and recurring orders, this setup could ultimately impact the B2B customer experience and therefore revenue.

2. B2B BNPL can be expensive and eat into your margins

Most BNPL providers charge a transaction fee which is typically higher than regular processing fees of debit cards (0.3-2%).

If your marketplace processes €1m each month through a BNPL provider that charges, say, 3% of the total transaction, you’re spending €300,000 per month just in processing costs.

As a marketplace, you can decide to either absorb this cost or pass it onto the buyer, for example by taking a small cut of each transaction or packaging the overall fees into a monthly platform subscription.

Note: In some setups, the processing cost can be passed onto the buyer as well, but this is much less common.

You’re now presented with a dilemma: charge buyers high fees that eat into their margins, or shrink margins of your own. Both options are less than ideal.

3. The buyer experience is disjointed, decreasing customer loyalty

When you integrate a BNPL payment option into your marketplace, you’re essentially adding a third-party provider into your checkout flow: and this means you’re giving up some control over how your buyers experience financing.

In certain older setups or simple integrations, buyers get redirected to the BNPL provider’s interface, where they apply for credit, confirm terms, and manage repayments under the provider’s own branding.

This leaves you at a disadvantage:

- Buyers move away from your platform at a critical buying moment, which adds friction to the payment experience and may cause drop-offs.

- Financing is presented as a third-party service rather than a seamless part of the marketplace business customer journey. Post-purchase interactions, for example, take place directly between the BNPL provider and the buyer. This can shift the buyer’s sense of loyalty and position you as a transaction facilitator, not a unified commerce partner.

- Buyer approvals and declines happen off your platform, limiting your visibility into the state of your own customers’ payment journeys.

To build higher customer loyalty, it’s ideal to turn financing into a value-added service under your own brand. But this isn’t possible with most BNPL solutions that are not API based.

In an ideal scenario, you want financing options that offer fast payouts to suppliers as well as later payment terms for buyers. Ideally, it should be embedded directly inside your platform without adding operational burden and without disrupting the buyer experience.

This is where embedded invoice financing comes in.

Why B2B marketplaces are turning to embedded invoice financing solutions like Aria

Embedded invoice financing has the pros of B2B BNPL – quick supplier payouts, payment on agreed terms for buyers, and outsourced risk – and solves the BNPL cons outlined above so that you can keep both suppliers and buyers satisfied.

Here’s how the financing process works with Aria, a financing solution that can be integrated directly into your marketplace and under your own brand:

- Buyers and sellers sign up and get onboarded through your platform while Aria automatically runs KYC/KYB verifications, credit checks, and risk assessments in the background.

- Once a buyer places an order, they agree to pay on their preferred terms, such as Net 30, 60, or 90.

- The supplier issues an invoice through your marketplace and decides if they want to finance it so they can receive an immediate payout.

- Aria runs instant risk and credit checks on the transaction (invisibly to the buyer) and validates the invoice.

Note: During this step, Aria underwrites the buyer, not the supplier. This means that eligibility for financing is based on the buyer’s creditworthiness rather than the supplier’s operating history or collateral, as would often be the case with traditional factoring. As a result, even small suppliers can access instant financing.

- Aria advances up to 100% of the invoice amount to the supplier depending on the buyers’ credit profile, usually within 24 hours.

- The supplier can see this directly inside your marketplace interface, with no third-party redirects.

- The buyer pays Aria on agreed terms. Aria takes on all credit risk and collection responsibilities, protecting your suppliers and your marketplace from default risk.

- Your platform receives real-time updates: which invoices are financed, which are paid, which are outstanding, and so on.

- Suppliers can also track every invoice, see expected payout dates, and view fees, allowing them full visibility into the buyer-seller relationship.

Instead of integrating a third-party BNPL provider in your checkout experience, you get to embed an invoicing workflow directly into your existing systems.

Why choose Aria as your embedded invoice financing partner

Buyers want to pay on their usual terms, suppliers want to be paid quickly, and you want to use your own funds to grow your business, not to relieve the tension between the two.

That’s why we built Aria, an embedded invoice financing solution that advances same-day funds to suppliers while B2B marketplaces get to invest working capital into scaling their operations.

With Aria, you get to outsource credit risk and payment collections, but without losing control of the customer journey. What’s more, your suppliers become active financing players so that they can make informed decisions on their B2B payments operations: all within your platform and under your brand.

Here’s why large marketplaces like Job & Talent, Malt and Staffme have decided to partner with us:

Finance small suppliers and offer payouts within 24 hours

As a marketplace, you depend on the performance of many small and mid-sized suppliers, who usually operate on tight cash reserves and rely on fast payouts to restock and keep up with demand.

Traditional factoring options rarely work for them: to issue a loan, banks require proof of long-operating histories, predictable cash flow, or collateral, which small merchants often don’t have. Even when they can qualify, the process is slow and full of paperwork.

As a result, these long-tail suppliers tend to rely on quick cash flow from your marketplace.

But funding hundreds or thousands of small invoices manually isn’t scalable. That’s why we designed Aria to automate the entire financing flow, from credit decisions to invoice validation and payments. With us, 99% of payments run automatically, and 92% of applicants receive instant decisions, enabling suppliers to access liquidity right when they need it.

Once a buyer confirms they’ve received the goods or services, Aria can pay the supplier within 24 hours and advance up to 100% of the invoice value. Buyers pay later on their usual terms, and Aria absorbs all repayment risk so that your marketplace stays protected.

And because Aria underwrites the buyer, not the supplier, even the smallest sellers on your platform can be offered instant financing.

We also enable you to create your own fee structure. It’s up to you to either absorb our fees as a free value-added service or to pass them onto the suppliers. For an invoice of €8,000, for example, we can charge the supplier 1.5% of the invoice value and advance the funds immediately at €7,800.

In the meanwhile, buyers can still pay on their regular payment terms (30, 60, or 90 days) and get extra breathing room to manage their cash flow.

Embed the invoice financing flow directly into your systems and scale confidently across 100+ countries

Once embedded, Aria runs behind the scenes, under your brand, without redirecting users to third-party sites and breaking UX – maintaining superior functionality throughout the payment experience.

Our simple REST API slots into your systems without forcing you to redesign your processes. And if you want to start smaller, you can use our manual dashboard before moving onto full automation when you’re ready.

As an all-in-one payment solution for invoice financing, risk management, and payments, Aria also removes the complexity of stitching together multiple integrations and contracts: instead of relying on separate vendors for KYC, risk checks, and collections, you get all you need through one API.

As you scale internationally, Aria can support you across over 100 countries, multiple currencies, and payment rails like SEPA, SCT, SWIFT, and FPS. Buyers also receive a single IBAN to simplify international payments.

With €2b in capacity and clients processing upwards of €200k transactions per month, Aria grows with you – directly from inside your payments infrastructure.

You’ll also have hands-on support, from a dedicated implementation manager to a key account manager, as well as direct access to our product and finance teams.

Protect against fraud with Aria’s compliance and risk management system

As marketplaces speed up payments with instant financing options, the risk of fraud increases: faster payouts mean fraudsters have a shorter window to exploit, and the more liquidity you offer, the more attractive your platform becomes to bad actors.

With Aria, you can securely onboard global users with automated KYC/KYB checks built directly into your onboarding flow.

You can also use our risk analysis system to automatically:

- Check solvency and recommended credit limits for each counterparty. With our technology, we only need a company registration ID to determine financing limits and advance funds.

- Protect against fraud with AI-powered tools that continuously scan for unusual patterns, such as sudden volume spikes or unexpected changes in account details.

- Track invoice validation in real-time through secure methods clickwrap and emails, helping you spot and solve potential disputes early on.

- Set custom thresholds that automatically flag suspicious transactions for manual review so that you can stop fraud before it impacts your platform.

These safeguards are built into your infrastructure, which means you get to stay compliant and protected without adding external vendors or tools as you scale.

How Aria’s flexible financing solutions helped UrbanChain achieve 10x growth to £25M in revenue

UrbanChain is a UK-based B2B marketplace that transforms the renewable energy landscape by connecting renewable generators directly with customers through local energy markets.

UrbanChain faced two challenges when they reached out to us: they struggled to manage cash flow during rapid expansion and to provide flexible financing options to a diverse portfolio of vendors.

While UrbanChain’s expanding base of larger B2B buyers demanded longer payment terms and was more complex to underwrite, their existing financing solutions couldn’t offer the flexibility they required for different vendors.

By partnering with Aria, UrbanChain was able to implement flexible and automated financing solutions that accommodated specific vendor needs. They also received personalised and direct team support, and could integrate Aria easily into a complex tech stack.

Since the partnership began, UrbanChain has achieved:

- 10x annual growth from £2.4 million to £25 million

- Higher credit limits for bigger clients, thereby expanding opportunities

- Streamlined invoice processing for large accounts (200-300 invoices at the same time)

- Enhanced cash flow management during quick expansion

- Built-in financing foundation that supports “limitless growth”

Read the full case study here: UrbanChain achieves 10X growth with Aria’s flexible financing solutions

Aria’s embedded invoice financing: Get the benefits of B2B BNPL, while offering a superior experience for everyone

B2B BNPL solutions can be a good starting point for B2B marketplaces that want to offer buyers flexible payment terms without doing the financing themselves. But as your platform grows, its limitations – from high processing fees to separate, buyer-centric workflows – start to hold you back.

Embedded invoice financing offers the same advantages as BNPL, but without the trade-offs. You can pay suppliers instantly, let buyers pay later, and eliminate credit risk while keeping the entire experience within your own platform.

With Aria, you get a financing partner that was built for B2B marketplaces. We enable you to keep your brand front and centre while we manage risk, protect against fraud, handle collections, and automate invoicing behind the scenes.

See how we can help you: Request a demo today.

FAQs: B2B BNPL

1. How does B2B BNPL work?

B2B BNPL is a payment method that lets business buyers purchase goods or services immediately and on deferred payment terms – usually 30, 60, or 90 days. While the supplier is paid on regular terms, the buyer repays the BNPL provider on the agreed schedule.

For B2B marketplaces, this means they don’t need to use their own capital to finance later payments, keeping buyers satisfied.

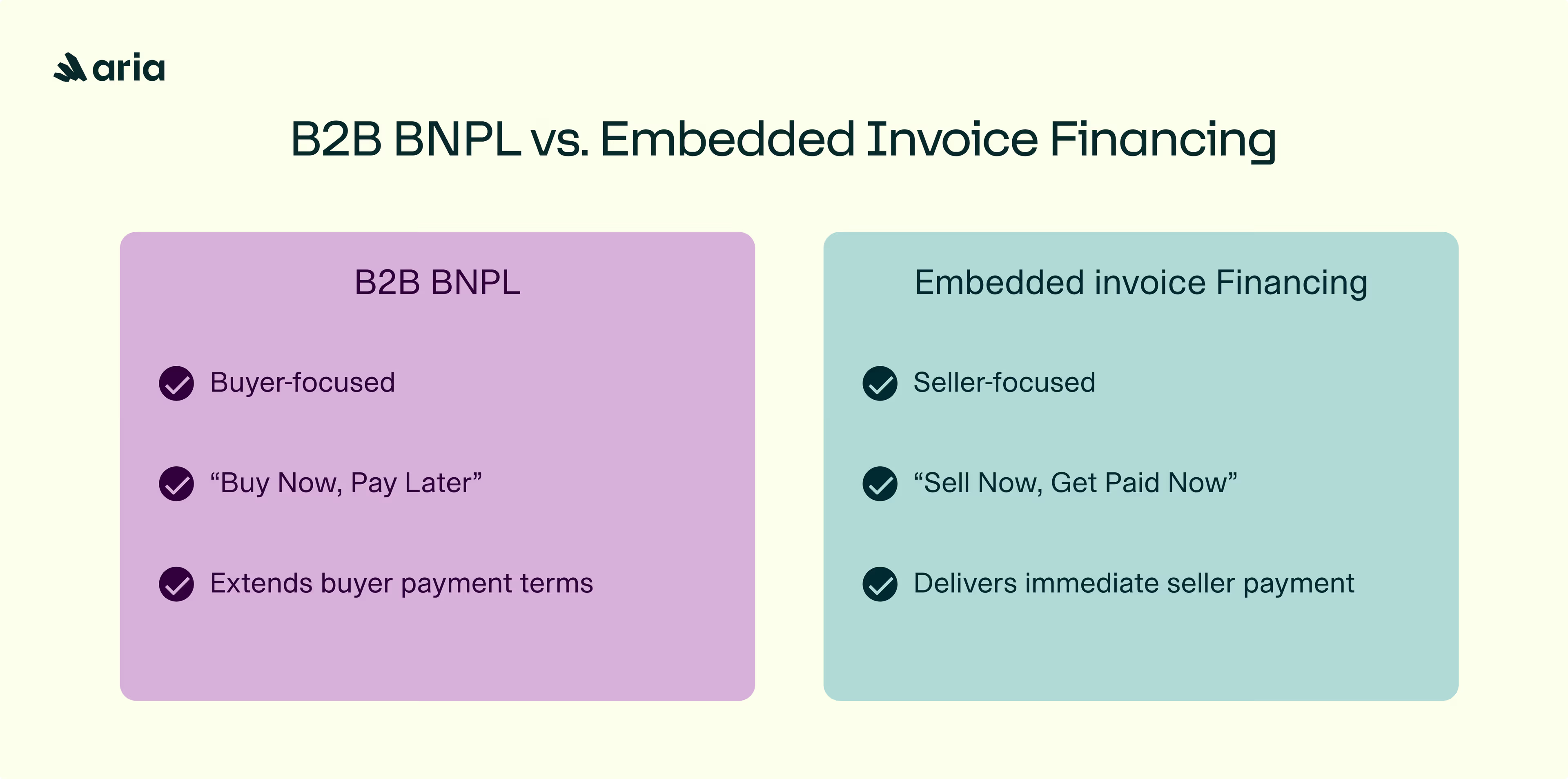

2. What’s the difference between B2B BNPL and embedded invoice financing?

While B2B BNPL is a buyer-centric payment method that redirects the buyer to a third-party service, embedded invoice financing is a model that’s integrated directly into the platform where buyers and suppliers connect. With embedded invoice financing, suppliers issue invoices, choose which ones to finance, and get paid quickly through the platform’s branded interface. At the same time, buyers get to keep their usual payment terms.

3. Who can use embedded invoice financing?

Any B2B marketplace, platform, or SaaS product that handles invoicing between buyers and suppliers can use embedded invoice financing. It’s especially valuable for platforms where suppliers need fast payouts, buyers prefer deferred payment terms, and transaction volumes are growing quickly.

Financing providers like Aria also make it possible to finance many small businesses through a B2B platform because Aria underwrites the buyer, not the supplier.